Charities

Tickets, events, raffles

HMRC has specific restrictions as to whether Gift Aid can be applied / claimed if the donor is receiving a 'benefit' in return for the donation (such as admission to an event, a raffle ticket, or an item purchased in an auction).

When donors make a donation to charity through Wonderful, they are given the option to apply Gift Aid, which allows the charity to claim an extra 25p for every £1 donated.

Donors, fundraisers and charities using the Wonderful platform should be aware of the rules around Gift Aid and how these rules apply to their particular fundraising event/campaign.

The HMRC guidance on Gift Aid Chapter 3.4.5 states:

Payments to a charity in return for services, rights or goods are not gifts to charity and so are not eligible for the Gift Aid Scheme. For example, the following cannot come within the Gift Aid Scheme:

payment for admission to events (jumble sales, concerts)

payment for raffle or lottery tickets (including 100 clubs) – the payment to purchase a raffle ticket from a charity is not a gift but a payment for the right to enter the raffle – it does not matter that the chance or expectation of winning a prize is small or that the prize is of little value

HMRC Gift Aid guidance

For more information, take a look at the official guidance below:

Gift Aid guidance for charities

Also see specific information on:

Selling tickets for a charity event

If you are unsure whether Gift Aid should be applied on a particular fundraising event/donation, please don't hesitate to contact us via the live chat button at the bottom of this screen.

05 · Resources

Featured FAQs

Have a look at these other articles that we think might interest you.

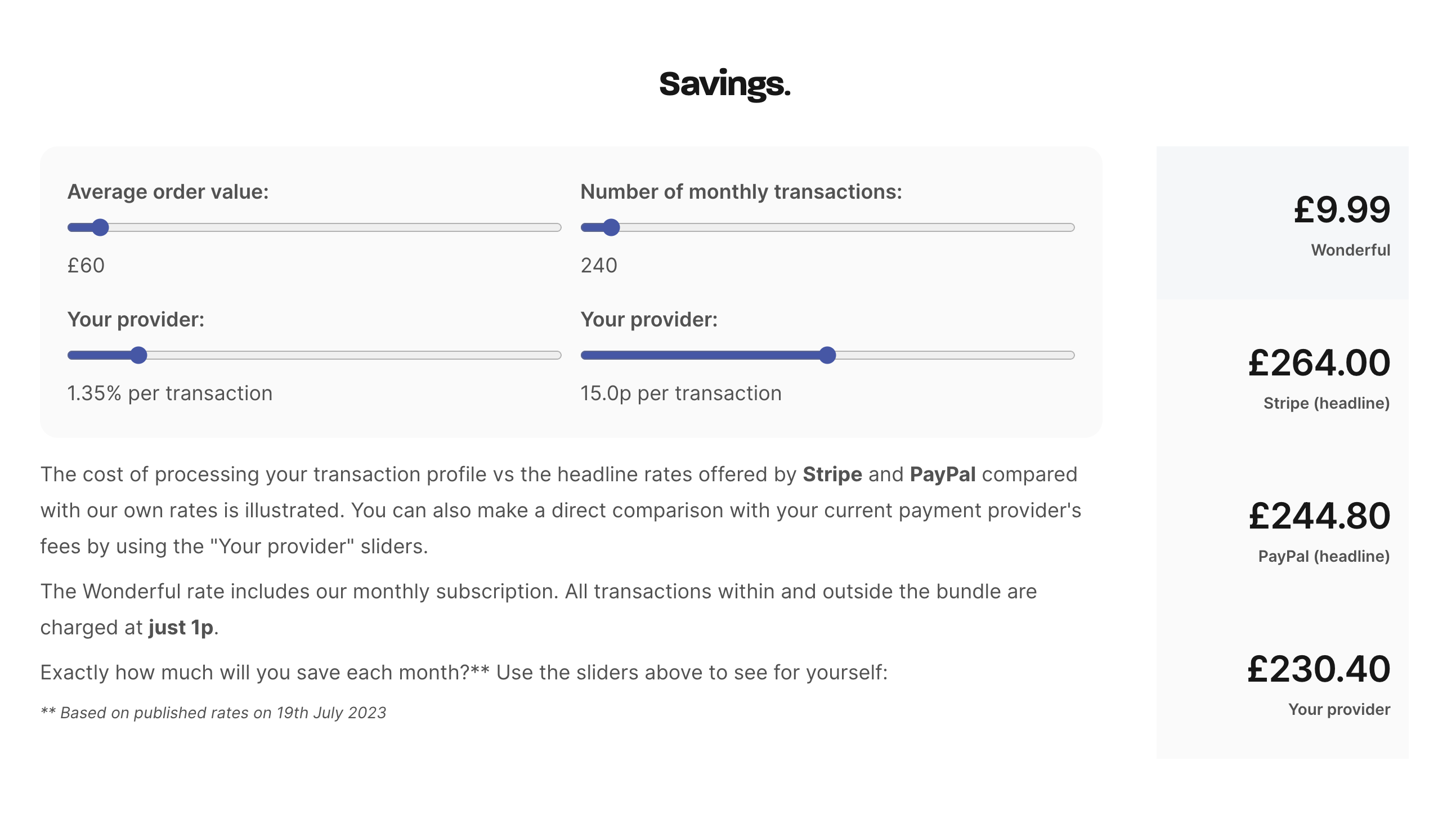

How much will I save?

Our highly predictable, transparent and aggressive fee structure, typically saving merchants more than 90% on transaction fees is a simple, secure alternative to debit and credit cards. It also includes instant settlement.

Enterprise integrations

Wonderful's instant bank payment service can be integrated with your checkout. Our public API will be released shortly. Contact our team to find out how much we can save your enterprise business on transaction processing fees.

Why we don't take cards

We do not take a percentage of funds raised, ask for tips, or do anything that prevents 100% of donations going to the causes that charity supporters are so passionate about. We are inspired and driven by that passion.